Simple 401k and 403b Facts

As a high school and even a College student I heard about 401ks and 403b’s but I never really knew what they consisted of.

Maybe you can relate.

Even as adults in the working world most of us still aren’t exactly sure how these retirement plans work.

My first “real job” when I graduated from college was working as entry-level IT support in an insurance firm, and I remember my first week on the Job to meet with the HR department to discuss retirement and other benefits options…

And let’s say there were a lot of head nods and “Ok’s”, I walked out of there and researched everything.

Asking myself what’s a 401k? Only to find that these retirement things are really important.

So let’s get on with it.

What Is A 401k Or A 403b?

Let’s start with an overview of what these plans are:

401k’s and 403b’s are employer retirement contribution plans, that allow employees in an organization to contribute pre-tax money to invest in stock and bond funds to provide an income in retirement.

401k plans and 403b plans are very similar, but they have slight differences.

401k plans are found in most organizations but you might have a 403b plan if you work in a government or non-profit organization.

Contributions

As of 2022, the contribution limit of the 401k/403b is as follows:

- $20,500 pre-tax a year for employees under 50 years of age

- An additional $6,500 pre-tax (called the catch-up limit) for employees ages 50 and up, for a total of $27,000 a year.

- For the 403b plan, if the employee stays with the organization for 15 or more years they are allowed an additional $3,000 pre-tax contribution, which brings the contribution limit up to $23,500 or $30,000 for employees age 50 or over.

Withdrawal

- You can withdraw funds from your 401k or 403b plan at age 59.5 or older and you will have to pay income tax on the withdrawal.

- If you are younger than 59.5 then you will have to pay a 10% penalty for early withdrawal and you will also have to pay income tax on the withdrawal.

- It is possible to withdraw early but it does come with a few rules, this is called rule 72(t) and it gets complex so please work with a financial advisor or tax professional before considering this step.

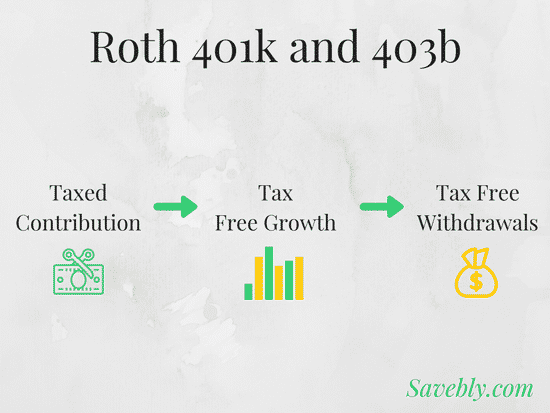

401k/403b VS Roth 401k/403b

401k’ s/403b’s also come in Roth form, meaning you pay taxes up front instead of paying taxes later

Simply:

And…

So which one is right for you, 401k or Roth 401k?

Well, it depends.

A good rule of thumb is that if you are in one of the lower tax brackets then it is more beneficial to put your money in a Roth 401k and if you are in a higher tax bracket then a 401k may be the better choice.

Now, this can get a bit complicated so it is best to contact your financial advisor and your HR department before making your decision. Let’s keep this simple for now.

6 Important Notes To Remember

- 401k plans typically have more fund options than a 403b.

- 403b funds are typically less expensive, meaning they have smaller expense ratios. For both the 401k and 403b aim for the mutual funds with the lowest fees.

- If you change employers you can roll over your 401k from your previous employer to your new employer’s 401k plan, also you can roll over your 401k into a 403b plan and vice versa. You can also choose to roll over your 401k/403b into an IRA/Roth IRA

- If your employer is offering a match to your 401k/403b contributions definitely contribute up to that limit, it is free money!

- Consider placing your contributions in a target date fund, which automatically balances your portfolio risk based on age. If you are not sure what your risk tolerance is then the target date fund is for you.

- Constantly check the IRS website for changes to the contribution limits and rules for 401k and 403b plans.

Conclusion

There we go, a simple explanation to answer the question: what’s 401k and 403b?

I know… I know, that was a lot to take in.

Now take this information in and start investing in your retirement plan early to take advantage of compound interest.

Make sure you are contributing to your retirement plan and set up an automatic withdrawal based on a percentage of your income (so if you get a raise you are also automatically investing more).

The more you are making in your career, the more you should be contributing to lower your taxable income.

Now set up your contributions and let your money grow!

Are you investing in a 401k or 403b?